The End of SAVE: The Next 90-Days are Critical for Borrowers

- Melissa Maguire

- Apr 15

- 2 min read

On April 1st, the U.S. Department of Education issued a major update to borrowers currently enrolled in the SAVE repayment plan.

The message was direct: “The SAVE Plan is ending. Borrowers must take action.”

While the announcement may seem straightforward, the details behind this transition are critical.

Here’s what borrowers need to understand and how to respond.

The 90-Day Window: What It Is and How It Works

One of the most important parts of the Department’s announcement is the introduction of a 90-day decision window, but understanding how this timeline works is key.

When Does the 90 Days Start?

The 90-day clock does not begin on April 1st.

Instead, there will be a formal notice sent that by your loan servicer that will include a specific deadline.

What You’re Expected to Do During the 90 Days

During this period, borrowers are expected to:

Review available repayment plan options

Compare monthly payments and long-term costs

Select a new repayment plan

Submit any required applications or income documentation

Taking action within this window allows you to actively choose a plan that aligns with your financial situation and long-term goals.

What Happens If You Don’t Take Action

If no plan is selected within the 90-day window:

You will be automatically placed into a different repayment plan

The plan will be assigned based on your loan type and circumstances

It is likely you will be placed on a Standard Repayment plan if there is no recent income documentation on file or no consent to access income information from the IRS on your behalf

The assigned plan may not be the lowest payment or best strategic option

Why This Window Matters More Than It Seems

While the Department describes this as “ample time,” there are several important considerations:

Timing varies by borrower: Not everyone will receive notice at the same time

Servicer delays are still common: Waiting too long could delay your enrollment

Plan approval is not always immediate: Some plans require processing time and documentation

Forgiveness strategies may be impacted: Especially for borrowers pursuing PSLF or long-term IDR forgiveness

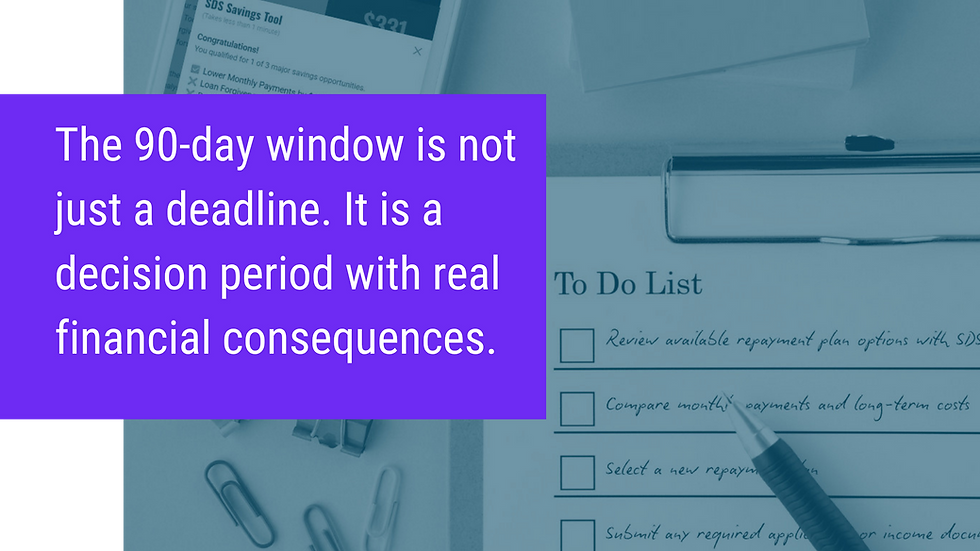

The 90-day window is not just a deadline. It is a decision period with real financial consequences.

Borrowers who act early maintain control over:

Their monthly payment amount

Their eligibility for forgiveness programs

Their total repayment cost over time

Relying on automatic placement removes that control.

What You Should Do Next

Watch for communication from your loan servicer

Understand when your 90-day window begins

Evaluate whether to act now or wait for new plan options

Avoid relying on automatic placement

Borrowers who take the time to evaluate their options now can:

Secure a more affordable monthly payment

Stay on track for forgiveness

Reduce long-term repayment costs

Log into Student Debt Solutions to review your loan status, model repayment options, and see recommended next steps based on these important rules.